Lend on Fund Ourselves Peer-to-Peer platform

Actual return may be higher or lower. Your capital is at risk. Investments are not protected by the FSCS. See key risks below.

Fund Ourselves Peer-to-peer Lending Features

At Fund Ourselves you lend directly to people who have applied for a loan on our platform. They get the funds they need, and you can earn returns as they pay you back each month.Your investment is lent to borrowers who match your selected risk zone and interest rate after borrowers pass our credit and affordability check .Types of lending offered We offer two types of investments, standard and IF ISA. They work in the same way, find out more about our IFISA here.

Auto-Diversify™ Each of your investments will be automatically lent to at least 5 available borrowers for each loan value from £100 to £1,500 diversifying your portfolio. Borrowers are shared by other investors as well.

Auto-Match™ feature We will automatically match your investment based on your pre-selected interest rate to matching borrowers within corresponding estimated interest rate risk zone.

Risk based interest returns

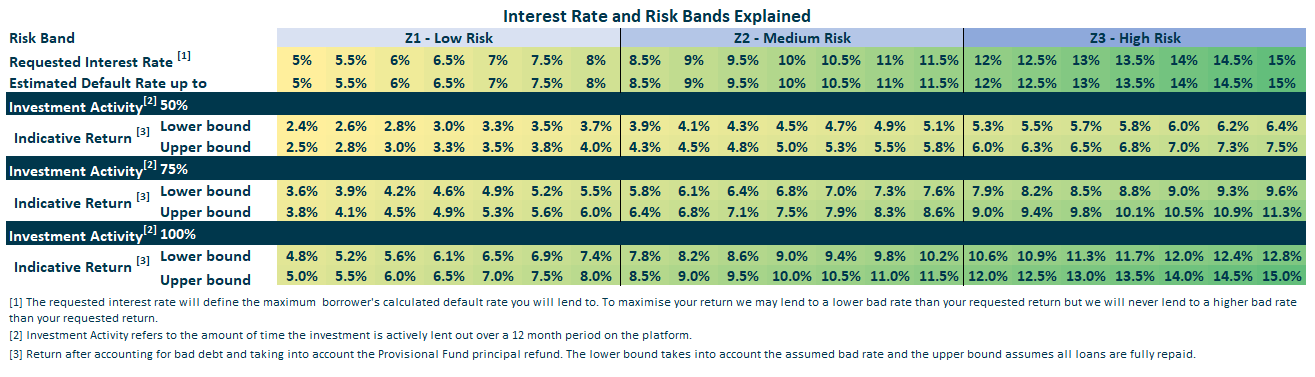

When lending through Fund Ourselves, you can earn maximum return chosen from 5% - 15%* interest per annum. This return is the maximum you can get assuming the investment is continuously lent out to matching borrowers over a 12-month period with no defaults.Interest rates are guided by the credit risk rating allocated to each loan. Higher-risk loans may yield greater returns but can also lead to lower returns if borrowers can’t fully repay their debts. Actual return may vary depending on pool time and loan defaults. See Risk Statement below.The interest rate you choose will determine the maximum borrower estimated default rate you will be lending to. For example, if you choose 10% return, you will be lending to borrowers with an estimated 10% chance of defaulting. The table below defines our estimated returns for each interest rate requested by our lenders.

The estimated returns presented above are before tax assuming continued lending over a 12 month period. Lenders may be liable for income tax on earned interest. To check if you are liable for income tax on your earned interest please check the HMRC website or seek professional advice.Fund Ourselves calculates the Probability of Default for each Risk Band based on objective data which is analysed by our in-house team of data scientists and analysts working full time supported by machine learning to create and update our credit policy and credit scoring regularly. Please see the Outcome Statement section below for more details.

NOTE:

Risk based interest rates are for estimation purposes only.Past performances and our forecast default rates are not a reliable indicator of future performance. Higher-risk loans may yield greater returns but can also lead to lower returns if borrowers can’t fully repay their debts.

Risk based interest rates are for estimation purposes only.Past performances and our forecast default rates are not a reliable indicator of future performance. Higher-risk loans may yield greater returns but can also lead to lower returns if borrowers can’t fully repay their debts.

Investment Withdrawal Process

You can request a withdrawal of your investment after logging into your online account with Fund Ourselves. Please note there are risks associated with withdrawal and the process can take time:Where the whole or any part of your investment has not been lent you will typically receive the funds within 7-10 working days.Where the funds have been lent, you must request a withdrawal of the entire lent amount (partial withdrawals of lent amounts are not permitted). Please also bear in mind:

- We will effect your withdrawal by seeing if there are other suitable investors to take on your loans in our secondary market. There may not be any and we cannot do this where borrowers are in arrears. If transfers can be achieved, you will typically receive the funds within 7-10 working days.

- Where we cannot find suitable investors willing to take on your loans or otherwise transfer your loans then we will wait for the loan terms to complete, pay you such sums as are due to you in the normal course of events rather than rolling your investment forward into new loans.

- We have a threshold before we make payments, so as to ensure that we are not burdening you by paying you very small amounts that are difficult to track, we shall make payments to you when the threshold is reached.

The provision fund we offer does not give you a right to a payment so you may not receive a pay-out even if you suffer loss. The fund has absolute discretion as to the amount that may be paid, including making no payment at all. Therefore, investors should not rely on possible pay-outs from the provision fund when considering whether or how much to invest.

Warning:

Fund Ourselves products are not covered by the Financial Services Compensation Scheme. Your capital is at risk. Higher returns are subject to higher default risks.

Fund Ourselves products are not covered by the Financial Services Compensation Scheme. Your capital is at risk. Higher returns are subject to higher default risks.

Key Risks on high-Risk P2P investments

Estimated reading time: 2 minDue to the potential for losses, the Financial Conduct Authority (FCA) considers this investment to be high risk.What are the key risks?1. You could lose the money you invest- Many peer-to-peer (P2P) loans are made to borrowers who can’t borrow money from traditional lenders such as banks. These borrowers have a higher risk of not paying you back.

- Advertised rates of return aren’t guaranteed. If a borrower doesn’t pay you back as agreed, you could earn less money than expected. A higher advertised rate of return means a higher risk of losing your money.

- These investments can be held in an Innovative Finance ISA (IFISA). An IFISA does not reduce the risk of the investment or protect you from losses, so you can still lose all your money. It only means that any potential gains from your investment will be tax free.

- Some P2P loans last for several years. You should be prepared to wait for your money to be returned even if the borrower repays on time.

- Some platforms may give you the opportunity to sell your investment early through a ‘secondary market’, but there is no guarantee you will be able to find someone willing to buy.

- Even if your agreement is advertised as affording early access to your money, you will only get your money early if someone else wants to buy your loan(s). If no one wants to buy, it could take longer to get your money back.

- Putting all your money into a single business or type of investment for example, is risky. Spreading your money across different investments makes you less dependent on any one to do well.

- A good rule of thumb is not to invest more than 10% of your money in high-risk investments. https://www.fca.org.uk/investsmart/5-questions-ask-you-invest

- If the platform fails, it may be impossible for you to collect money on your loan. It could take years to get your money back, or you may not get it back at all. Even if the platform has plans in place to prevent this, they may not work in a disorderly failure.

- The Financial Services Compensation Scheme (FSCS), in relation to claims against failed regulated firms, does not cover investments in P2P loans. You may be able to claim if you received regulated advice to invest in P2P, and the adviser has since failed. Try the FSCS investment protection checker here. https://www.fscs.org.uk/check/investment-protection-checker/

- Protection from the Financial Ombudsman Service (FOS) does not cover poor investment performance. If you have a complaint against an FCA-regulated platform, FOS may be able to consider it. Learn more about FOS protection here. https://www.financial-ombudsman.org.uk/consumers

Other Key investment Risks

Fund Ourselves works hard to reduce risks associated with lending, however lending to unsecured to lending to unsecured borrowers with peer-to-peer lending platform like Fund Ourselves, it’s important to remember that your capital and interest is at risk.Here are key risks lenders should be aware of:Fund Ourselves products are not covered by the Financial Services Compensation Scheme. Your capital is at risk. Higher returns are subject to higher default risks.Bad DebtsIt's important to remember that a borrower may not be able to fully repay its loan. This is known as bad debt and while we have a collection system in place, you may not receive all the money you lent.Access to your investmentsPlease remember that the time taken to access your funds depends on how quickly your holdings are sold. The ability to sell depends on other lenders buying your loans, and the borrowers not being late on their payments. Please see investment withdrawal process.TaxLenders are responsible for ensuring that they administer their own tax affairs and should seek independent financial advice. Fund Ourselves doesn’t provide tax advice and lenders are responsible for completing their own tax return.Tax treatment depends on the individual circumstances of each lender and may be subject to change in future.No interest if investments not lent outIt’s important that lenders understand that even if money is loaded to the Fund Ourselves platform, it won’t earn interest unless it’s lent to borrowers.What Do We Do To De-risk Your Investments?

Borrowers' Creditworthiness

We do extensive checks on our borrowers to verify their creditworthiness before issuing any loans. Firstly, we carry out background checks like identity, fraud and anti-money laundering (AML). Once cleared, applicants are credit scored and their affordability is checked to determine their creditworthiness which is the final stage to determine if a borrower is approved or rejected.Dealing with defaults

Our credit assessment and affordability checks allow us to gain prediction of the borrowers’ likelihood of defaulting. We aim to achieve our target average default rate of 15% by being selective of who we accept as a borrower on our platform.In the event we see our average default rate going higher than our target average default rate, we may close the lending door to riskier borrowers by tightening our credit assessment and affordability criteria.If a borrower fails to repay the instalment within 35 days of it becoming due, we will report the non-payment to the credit reference agency. Thereafter, our collections teams and external recovery provider commence the process to recover the amount outstanding.Provision Fund

The provision fund we offer does not give you a right to a payment so you may not receive a pay-out even if you suffer loss. The fund has absolute discretion as to the amount that may be paid, including making no payment at all. Therefore, investors should not rely on possible pay-outs from the provision fund when considering whether or how much to invest.

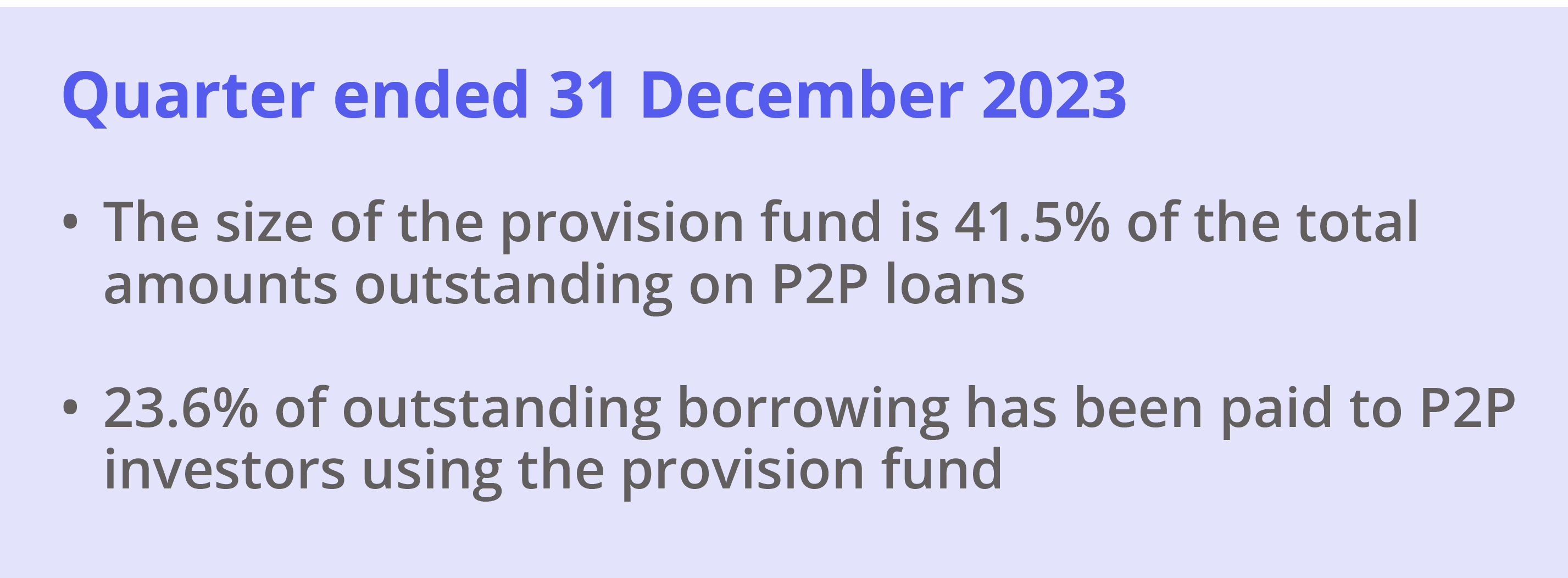

For an additional layer of stability, we created the Provision Fund which aims to cover investments of our peer-to-peer investors. It does not cover any other current of future lending products we may offer.Borrowers who take out a loan from Fund Ourselves Platform pay interest on the money that they have borrowed. Part of the interest goes to the investor; part covers the operational fee of our P2P platform, and a part goes into the Provision Fund. Funds in the Provision Fund are segregated funds which aims to reimburse the principal amount lost to the investors in the event the borrower fails to meet their repayments. The Provision Fund changes along with the portfolio size and repayments made by borrowersIn the event where the Provision Fund was not able to pay you back for your loss, any funds bad debt collected by the internal collections team is transferred to you.The Provision Fund is a buffer to protect your investment which is not a guarantee; however, it aims to reimburse all our lenders for their principal losses subject to fund availability. Your capital and interest are at risk if the Provision Fund is depleted by increased borrower defaults. Please see our Provision Fund policy here for further details.Provision Fund Performance

Table for actual funds (segregated funds kept aside) by quarter.Please note that Past performances and our forecast of borrower risk rate might not be a reliable indicator of future results.

Fund Ourselves P2P Outcome Statement

In line with the FCA regulations, Fund Ourselves publishes the outcome statement each year.The Outcome Statement shows performance of all Peer-to-Peer (P2P) loans that we have facilitated on The FundOurselves platform, the expected and actual default rates by Risk Band and the actual return over the each financial year against any target rate published.We are required to publish an outcomes statement within four months of the end of our financial year. Our financial year ends on 31 December. Outcome Statement 2023

Outcome Statement 2023Warning:

Please note the figures refer to the past and that past performance is not a reliable indicator of future result. When lending to unsecured borrowers, it’s important to remember that your capital is at risk. Fund Ourselves and its products are not covered by the Financial Services Compensation Scheme.

Please note the figures refer to the past and that past performance is not a reliable indicator of future result. When lending to unsecured borrowers, it’s important to remember that your capital is at risk. Fund Ourselves and its products are not covered by the Financial Services Compensation Scheme.

We continually monitor our outcomes and continue to enhance our credit risk rules and policy to get the best outcome for all parties.

Wind down plan

We are not planning to wind down and not foreseeing any reasons to wind down in the near future. However, if we are to wind down, we have a plan so it can be done smoothly and with the least effect on investments and the performance of live loans.In the event of a wind down, first we will close the door to all new investments and return all monies waiting to be lent back to lenders. We will also stop all marketing activities and will reduce the team size to what is required to support live loans to manage the repayments as planned and without disruption. The provision fund will continue to support the bad debt during the wind down process as it would normally during normal operations. The provision fund will be the last business unit to wind down once all loan agreements are settled or terminated.Again, this is our plan just in case we need it.

How it works?